Tally ERP 9 Lesson 1 - Basics of Accounting by Sujan Show

Lesson 1: Basics of Accounting

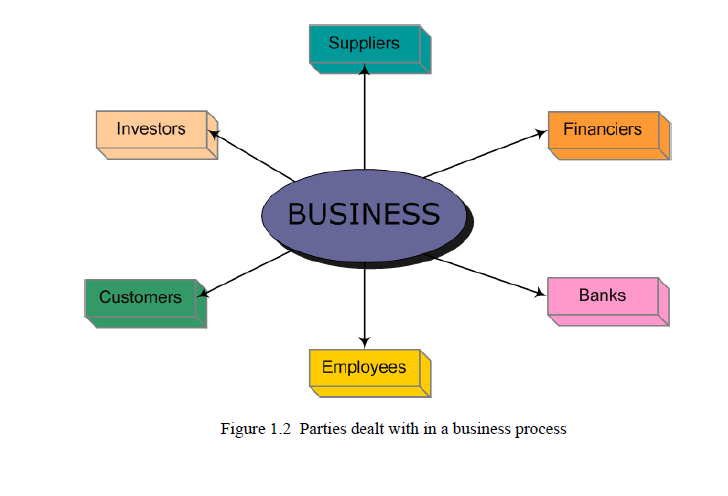

1.1 Introduction

Accounting is a process of identifying, recording, summarising and reporting economic informationto decision makers in the form of financial statements. Financial statements will be useful to

the following parties:

Suppliers

Customers

Employees

Banks

Suppliers of equipments, buildings and other assets

Lenders

Owners

1.1.1 Types of Accounts

There are basically three types of Accounts maintained for transactions : Real Accounts

Personal Accounts

Nominal Accounts

Real Accounts are Accounts relating to properties and assets, which are owned by the business

concern. Real accounts include tangible and intangible accounts. For example,

Land

Building

Goodwill

Purchases

Cash

Personal Accounts

Personal Accounts are Accounts which relate to persons. Personal Accounts include the following.

Suppliers

Customers

Lenders

Nominal accounts

Nominal Accounts are Accounts which relate to incomes and expenses and gains and losses of a

business concern. For example,

Salary Account

Dividend Account

Sales

Accounts can be broadly classified under the following four groups.

Assets

Liabilities

Income

Expenses

The above classification is the basis for generating various financial statements viz., Balance

Sheet, Profit & Loss A/c and other MIS reports. The Assets and liabilities are taken to Balance

sheet and the Income and Expenses accounts are posted to Profit and Loss Account.

1.1.2 Golden Rules of Accounting

1.1.3 Accounting Principles, Concepts and Conventions

The Accounting Principles, concepts and conventions form the basis for how business transactionsare recorded. A number of principles, concepts and conventions are developed to ensure

that accounting information is presented accurately and consistently. Some of these concepts are

briefly described in the following sections.

Revenue Realisation

According to Revenue Realisation concept, revenue is considered as the income earned on the

date, when it is realised. As per this concept, unearned or unrealised revenue is not taken into

account. This concept is vital for determining income pertaining to an accounting period. It

reduces the possibilities of inflating incomes and profits.

Matching Concept

As per this concept, Matching of the revenues earned during an accounting period with the cost

associated with the respective period to ascertain the result of the business concern is carried out.

This concept serves as the basis for finding accurate profit for a period which can be distributed to

the owners.

Accrual

Under Accrual method of accounting, the transactions are recorded when earned or incurred

rather when collected or paid i.e., transactions are recorded on the basis of income earned or

expense incurred irrespective of actual receipt or payment. For example, a seller bills the buyer at

the time of sale and treats the bill amount as revenue, even though the payment may be received

later

Going ConcernThe cash basis of accounting is a method wherein revenue is recognized when it is actually received, rather than when it is earned. Expenses are booked when they are actually paid, rather than when incurred. This method is usually not considered to be in conformity with accounting principles and is, therefore, used only in select situations such as for very small businesses.

As per this assumption, the business will exist for a long period and transactions are recorded

from this point of view.

Accounting Period

The users of financial statements required periodical reports to ascertain the operational and the

financial position of the business concern. Thus, it is essential to close the accounts at regular

intervals. viz., 365 days or 52 weeks or 1 year is considered as the accounting period.

Accounting Entity

According to this assumption, a business is considered as a unit or entity apart from its owners,

creditors and others. For example, in case of a Sole Proprietor concern, the proprietor is treated

to be separate and distinct from the business, which he controls. The proprietor is treated as a

creditor to the extent of his capital and all the business transactions are recorded in the books of

accounts from the business stand point.

Money Measurement

In accounting, only business transactions and events of financial nature are recorded. Only transactions that can be expressed in terms of money are recorded.

1.1.4 Double Entry System of Book Keeping

As per Double Entry System of book-keeping, all the business transactions recorded in accountshave two aspects - Debit aspect (receiving) and Credit aspect (giving). For example, when a

business acquires an asset (receiving) and pays cash (giving) for it. This accounting technique

records each transaction as debit and credit, where every debit has a corresponding credit and

vice versa.

Features of Double Entry System of Book Keeping

The Double entry system of book keeping comprises of the following features :

Every business transaction affects two accounts

Each transaction has two aspects, i.e., debit and credit

Maintains a complete record of all business transactions

Helps to check the accuracy of the accounting transactions, by preparation of trial balance

Helps ascertaining profit earned or loss occurred during a period, by preparation of Profit &

Loss Account

Helps ascertaining financial position of the concern at the end of each period, by preparation

of Balance Sheet

Helps timely decision making based on sufficient information

Minimizes the possibilities of fraud due to its systematic and scientific recording of business

transactions

The following chart explains the way in which accounting transactions are recorded in the Double

Entry system and financial statements are prepared.

1.1.5 Mode of Accounting

Accounting process begins with identifying and recording the transactions in the books ofaccounts i.e., the first step in the Accounting Process is recording of transactions in the books of

accounts. Accounting identifies only those transactions and events which involves money and is

sorted based on various source documents.

The following are the most common source documents.

Cash Memo

Invoice or Bill

Vouchers

Receipt

Debit Note

Credit Note

Voucher

A voucher is a document in support of a business transaction, containing the details of such transaction.

Receipt

When a trader receives cash from a customer against goods sold by him, issues a receipt containing

the name of such customer, details of amount received with date.

Invoice or Bill

When a trader sells goods to a buyer, he prepares a sales invoice containing the details of name

and address of buyer, name of goods, amount and terms of payments and so on. Similarly, when

the trader purchases goods on credit receives a Invoice/bill from the supplier of such goods.

Journals and Ledgers

A journal is a record in which all business transactions are entered in a chronological order. A

record of a single business transaction is called a journal entry. Every journal entry is supported

by a voucher, evidencing the related transaction.

Account

An account is a statement of transactions affecting any particular asset, liability, expense or

income.

Ledger

A Ledger is a book which contains all the accounts whether personal, real or nominal, which are

entered in journal or subsidiary books.

Chart of Accounts

A chart of accounts is a list of all accounts used by an organisation. The chart of accounts also

displays the categorisation and grouping of its accounts.

Posting

Posting is the process of transferring the entries recorded in the journal or subsidiary books to

the respective accounts opened in the ledger i.e., grouping of all the transactions relating to a particular account to a single place.

Accounting Period

Generally, the financial statements are generated for a regular period such as a quarter or a year,

for timely and accurate ascertainment of operating and financial position of the organisation.

Trial Balance

Trial balance is a statement which shows debit balances and credit balances of all Ledger

accounts. As per the rules of double entry system, every debit should have a corresponding credit, the total of the debit balances and credit balances should agree. A detailed trial balance

has columns for

Account name

Debit balance

Credit balance

1.1.6 Financial Statements

Financial statements are final result of accounting work done during the accounting period.Financial statement serves a significant purpose to users of accounting information in knowing

about the profitability and financial position of the organization. Financial statements normally

include

Trading

Profit and Loss Account

Balance Sheet

Trading Account

Trading refers to buying and selling of goods. The trading account displays the transactions pertaining

to buying and selling of goods.

The difference between the two sides of the Trading Account indicates either Gross Profit or

Gross Loss. If the credit side total is in excess of the debit side total, the difference represents

Gross Profit. On the other hand, if the total of the debit side is in excess of the credit side total, the

difference represents Gross Loss. Such Gross Profit / Gross Loss is transferred to Profit & Loss

Account. The Gross Profit is expressed as :

Gross Profit = Net Sales – Cost of Sales

Profit and Loss AccountThe profit and loss account helps to ascertain the net profit earned or net loss suffered during a

particular period. after considering all other incomes and expenses incurred over a period. This

helps the company to monitor and control the costs incurred and improve its efficiency. In other

words, the profit and loss statement shows the performance of the company in terms of profits or

losses over a specified period.

The Net Profit is expressed as :

Net Profit = (Gross Profit + Other Income) – (Selling and Administrative Expenses + Depreciation + Interest + Taxes + Other Expenses)

is that the amounts shown on the statement represent transactions over a period of time, while

the items represented on the balance sheet show information as on a specific date.

All revenue and expense accounts are closed once the profit and loss account is prepared. The

Revenue and Expenses accounts will not have an opening balance for the next accounting

period.

Balance Sheet

The balance sheet is a statement that summarises the assets and liabilities of a business. The

excess of assets over liabilities is the net worth of a business. The balance sheet provides information

that helps in assessing

A company’s Long-term financial strength

A company’s Efficient day-to-day working capital management

A company’s Asset portfolio

A company’s Sustainable long-term performance

The balances of all the real, personal and nominal (capital in nature) accounts are transferred

from trial balance to balance sheet and grouped under the major heads of assets and liabilities.

The balance sheet is complete when the net profit/ loss is transferred from the Profit and Loss

account.

1.1.7 Transactions

A transaction is a financial event that takes places in the course or furtherance of business andeffects the financial position of the company. For example, when you deposit cash in the bank,

your cash balance reduces and bank balance increases or when you sell goods for cash, your

cash balance increases and your stock reduces.

Transactions can be classified as follows :

Receipts – cash or bank

Payments – cash or bank

Purchases

Sales

1.1.8 Recording Transactions

The important aspect of accounting is to record transactions promptly and correctly to ascertainthe financial status of a company as on a particular date.

Generally, the business transactions may be of the folowing nature :

Purchase of goods either as raw materials for processing or as finished goods for resale

Payment of expenses incurred towards business

Sale of goods or services

Receipts (in Cash or by Cheques)

Payments (in Cash or Cheques)

The Accounting information is useful to various interested parties, both internal and external viz.,

Suppliers, who supply goods and services for cash or on credit

Customers, who buy goods or services for cash or on credit

Employees, who provide services in exchange of salaries and wages.

Banks, with whom accounts are maintained

Suppliers of equipment, buildings and other assets needed to carry on the business.

Lenders from whom, you borrow money to finance your business

Owners, who hold a share in the capital of your business

Points to Remember

Accounting is a comprehensive system to collect, analyse and communicatefinancial information.

Double Entry accounting is a system of recording transactions in a way that maintains the equality of the accounting equation.

The three types of accounts maintained for transactions are real

accounts, personal accounts and nominal accounts.

Entity is the organizational unit for which accounting records are maintained.

Journal entry is a record of a single business transaction.

Voucher is a document evidencing the details of a financial transaction.

Ledger is a book in which accounts are maintained.

Trial balance is a list of the balances of all the ledger accounts.

Profit and loss statement shows the performance of the company in terms of profits or losses made by it over a specified period.

Balance sheet gives an overview of the financial position of a company as on a specific date.

Lesson 2: Fundamentals of Tally.ERP 9 - Click Here

আমি তোমাদের সাইটে বিজ্ঞাপন দিতে চাই। আমার সাথে যোগাযোগ করুন ০১৬৪০০৬২৪৭৪

ReplyDeleteঅথবা imranwebco274@gmail.com

Thank You and I have a nifty give: Who Repairs House Windows Near Me exterior makeover house

ReplyDelete